Redefining value:

From style category to

investment discipline

March 2026

The traditional separation of value and growth implies two distinct styles with different return profiles, yet companies themselves evolve as earnings trajectories, capital allocation decisions, and valuation regimes change. Benchmark construction reinforces this fluidity, with meaningful overlap between growth and value indexes underscoring that style is a classification convention rather than a durable economic identity. At Boston Partners, we distinguish durable value from superficial cheapness through a broader assessment of business quality, cash-flow resilience, and capital allocation discipline—paired with a sell framework designed to mitigate value traps and respond as fundamentals shift.

The spectrum of value and growth

The investment industry conventionally frames growth and value as opposing styles—distinct categories that imply different philosophies, factor exposures, and expected return profiles. Asset allocation models, consultant databases, and manager lineups are often built around this divide. Yet the lived reality of equity markets is far less binary. Growth and value are not mutually exclusive economic identities; they are interpretive lenses applied to companies whose fundamentals, valuations, and expectations evolve over time.

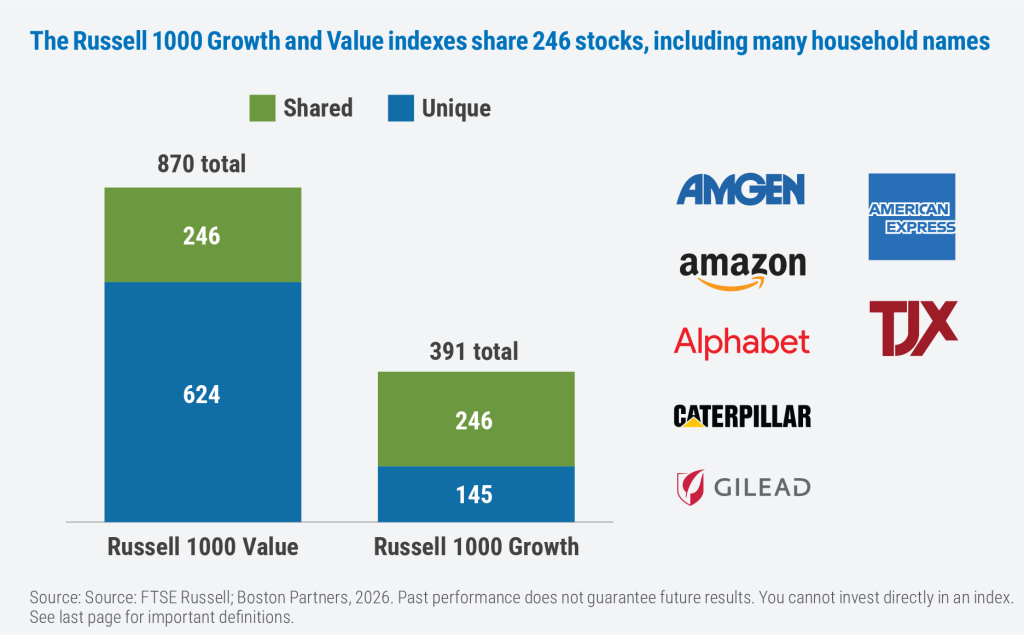

This fluidity is visible within the construction of major benchmarks. The Russell 1000 Value Index and the Russell 1000 Growth Index are widely used to represent the two style universes across large U.S. companies. However, index methodology permits meaningful overlap between them. Constituents are not permanently assigned to a single economic camp; rather, they are scored along a continuum of characteristics, which can result in partial inclusion across style segments. The implication is straightforward but important: even at the benchmark level, the growth-value divide is porous by design.

At the end of 2025, nearly 250 companies were constituents of both the Russell 1000 Value Index and the Russell 1000 Growth Index, including many household names with meaningful allocations in each index. These are not incidental inclusions; they represent economically meaningful exposures within both style constructs.

The structural takeaway is clear: Growth and value are not mutually exclusive economic categories but overlapping classification frameworks applied to the same underlying businesses. Businesses such as Alphabet, Amazon, and Meta are often labeled “growth” by default, as if they were growth archetypes. Yet their profitability profiles, free cash flow generation, and capital return policies increasingly resemble traits historically associated with value. Conversely, companies like Coca-Cola and American Express, commonly characterized as value archetypes, have demonstrated durable earnings expansion and pricing power more typically linked to growth narratives. Even a semiconductor innovator such as Advanced Micro Devices may simultaneously exhibit high forward growth expectations and valuation dynamics that shift its style classification over time.

The concept of “drift” must therefore be evaluated in context. At what point does deviation from a style label constitute a breach of mandate—and at what point is it a rational response to changing economic conditions? More importantly, when does apparent “drift” simply reflect the consistent application of an investment philosophy designed to underwrite key fundamentals—such as valuation discipline, earnings durability, balance sheet strength, and wise capital allocation—whose evolution naturally alters a company’s surface-level style profile? In that light, what appears as stylistic movement may, in fact, be evidence of process discipline rather than process breakdown.

What appears as stylistic movement may, in fact, be evidence of process discipline rather than process breakdown.

How we define value

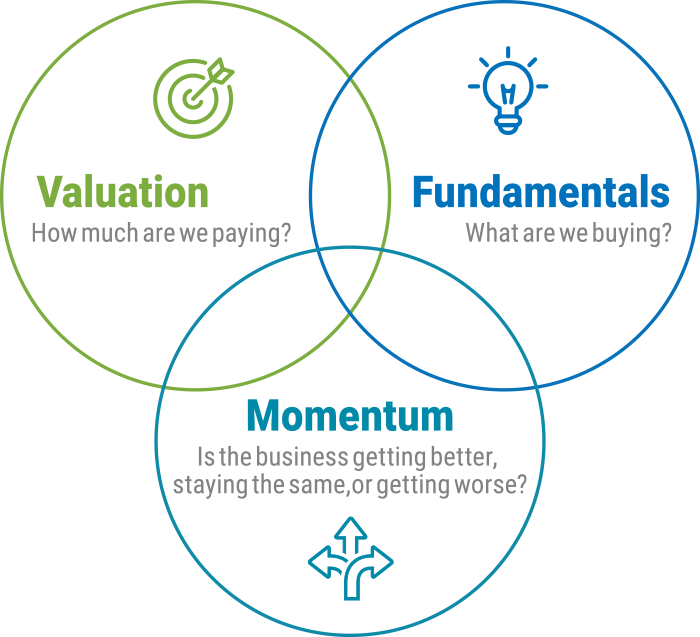

Not all stocks that screen as “value” necessarily represent compelling value. As we have noted elsewhere, our research highlights the limitations of relying too heavily on static price multiples as a primary investment criterion. Such approaches can increase exposure to “value traps”—businesses that appear inexpensive but lack the fundamental trajectory required to unlock that discount. For that reason, we focus on identifying companies where attractive valuation is supported by durable fundamentals and improving operating momentum, rather than price alone. Our Three Circle approach to investing, as we call it, has value as a defining characteristic, but our decision-making is driven by a multifaceted analysis of investment potential.

During periods of market stress or style rotation, valuation gaps can close rapidly. When they do, two-circle stocks can transition into actionable three-circle investments, which we remain prepared to move on with speed and conviction. This structure enables us to act decisively when volatility creates dislocations—regardless of whether the market temporarily categorizes those businesses as “growth” or “value.” In environments where style leadership can rotate abruptly, that flexibility is not cosmetic; it is essential to maintaining return discipline without sacrificing opportunity.

Beyond the style box

At Boston Partners, we are genuine value managers. That characterization reflects our respect for valuation discipline, but it does not fully describe our process. The integration of three distinct but interdependent dimensions—valuation, fundamentals, and momentum—must align to support a compelling, investable thesis.

Companies can remain inexpensive for structural reasons. Conversely, high-quality franchises can compound intrinsic value for extended periods before appearing optically cheap. Momentum, when unsupported by underlying business strength, can prove transient. Each dimension in isolation is incomplete. What matters is the intersection.

We believe durable returns across market cycles are more likely when a business demonstrates fundamental resilience, trades at a reasonable valuation relative to its prospects, and exhibits improving market recognition. The alignment of those three factors creates a reinforcing dynamic: fundamentals underpin conviction, valuation frames risk and return asymmetry, and momentum reflects the tangible evidence of a business’ stagnation or dynamism. Together, they form a disciplined framework for underwriting change beyond style labels and for compounding capital as businesses evolve.

Important information

The views expressed in this commentary reflect those of the author as of the date of this commentary. Any such views are subject to change at any time based on market and other conditions and Boston Partners disclaims any responsibility to update such views. Past performance is not an indication of future results.

Discussions of securities, market returns, and trends are not intended to be a forecast of future events or returns. You should not assume that investments in the securities identified and discussed were or will be profitable.

Terms and definitions

Factor exposures refer to observable drivers of return—such as value, size, and quality—beyond traditional classifications. Free cash flow generation is the total cash generated from operations minus capital expenditures. The Russell 1000 Value index tracks the performance of those large-cap U.S. equities in the Russell 1000 index with value style characteristics. The Russell 1000 Growth index tracks the performance of the large-cap U.S. equities in the Russell 1000 Index with growth style characteristics. It is not possible to invest directly in an index.

Boston Partners Global Investors, Inc. (Boston Partners) is composed of three divisions, Boston Partners, Boston Partners Private Wealth, and Weiss, Peck & Greer (WPG) Partners, and is an indirect, wholly owned subsidiary of ORIX Corporation of Japan (ORIX).

8806857.1

Large Cap Value

Our flagship U.S. equity strategy targeting attractively valued large-cap companies.